Statistical Rigor in Disaster Metrics: Toward a Global Framework for Climate Solvency

Integrating Catastrophe Analytics into Financial Regulatory Architectures as a Systemic Stability Imperative.

RN

RNThe contemporary financial architecture is undergoing an analytical transition comparable to the implementation of the Basel III accords, yet the driver of this shift is not merely traditional credit or market risk, but the technical quantification of natural disasters. The emergence of standardized "catastrophe accounting" is evolving from an isolated risk management tool into the fundamental pillar of climate-exposed solvency. Just as capital and liquidity ratios redefined banking resilience following the 2008 crisis, the systematization of disaster statistics is surfacing as the new compliance protocol for internalizing biophysical externalities within both sovereign and corporate balance sheets.

This technical evolution necessitates a departure from static probability models toward dynamic stochastic modeling that captures the inherent non-linearity of extreme events. The historical absence of a unified taxonomy and granular datasets has fostered information asymmetries that impede the accurate valuation of assets and liabilities. Consequently, the adoption of loss-and-damage reporting protocols under international standards allows disaster risk to become fungible and comparable across disparate jurisdictions. This technical convergence facilitates a "Climate Basel III" environment, where the transparency of loss data acts as a systemic safeguard, compelling institutions to maintain capital buffers proportional to their probabilistic exposure to hydrometeorological and geophysical phenomena.

The implementation of these data-driven regulatory frameworks shifts the perception of risk from the periphery of social responsibility to the core of financial engineering. Analyzing time-series disaster data, adjusted for vulnerability and exposure variables, enables the structuring of sophisticated risk-transfer instruments, such as catastrophe bonds and parametric insurance. Ultimately, the formalization of disaster statistics serves more than an elective informative function; it establishes a new paradigm of economic governance where resilience is measured through metric precision and capital adequacy in the face of climatic uncertainty.

Te puede interesar

El Clima como la Sexta C del Crédito: El Desafío de su Integración en Argentina e Iberoamérica

RN

Finanzas sostenibles28 de julio de 2026La evaluación tradicional de riesgo financiero ha quedado incompleta ante la aceleración de los eventos climáticos extremos. En Argentina y el Cono Sur, la incorporación del factor ambiental en las decisiones de inversión corporativa y municipal exige metodologías avanzadas, donde la articulación público-privada se consolida como un pilar estratégico.

Paradigmas en el Escalamiento Financiero: De la Innovación Territorial a la Inversión Estructurada

Peter Sundheimer

Finanzas sostenibles27 de julio de 2026Frente a la creciente brecha de infraestructura en América Latina, la integración de garantías de primera pérdida, financiamiento combinado y esquemas de transferencia de riesgo se consolida como la clave para transformar proyectos piloto locales en activos financiables de gran escala.

El Capital Natural en Llamas: Un Análisis Económico y Contable de los Incendios Forestales en Europa

RN

Finanzas sostenibles26 de julio de 2026Tras las evacuaciones masivas en España y Francia, la gestión territorial exige superar la retórica contemplativa e integrar la pérdida del activo natural, los costos de reposición de infraestructura crítica y los pasivos de salud en la contabilidad estatal.

Democratización del Capital Climático: La Tokenización de Activos Reales como Palanca para la Transición Energética en el Mercosur

RN

Finanzas sostenibles26 de julio de 2026Cómo los retornos denominados en bienes esenciales y los nuevos marcos normativos de la CNV abren la inversión en infraestructura verde a los presupuestos de los hogares en Argentina y Brasil.

Lo más visto

Paradigmas en el Escalamiento Financiero: De la Innovación Territorial a la Inversión Estructurada

Peter Sundheimer

Finanzas sostenibles27 de julio de 2026Frente a la creciente brecha de infraestructura en América Latina, la integración de garantías de primera pérdida, financiamiento combinado y esquemas de transferencia de riesgo se consolida como la clave para transformar proyectos piloto locales en activos financiables de gran escala.

La paradoja del auge digital: El estrés hídrico de la infraestructura de datos y la transición hacia la refrigeración líquida

RN

Ciencia e Innovación27 de julio de 2026El crecimiento acelerado de la inteligencia artificial y el procesamiento intensivo exige repensar los modelos térmicos tradicionales ante la escasez crítica de agua dulce y las eventualidades climáticas extremas.

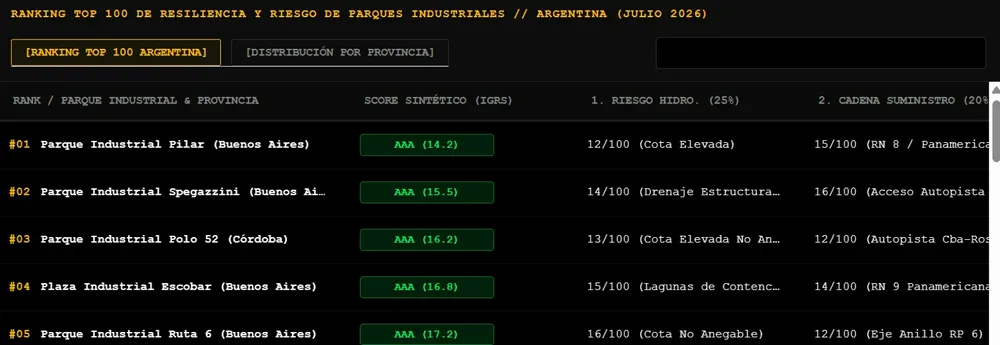

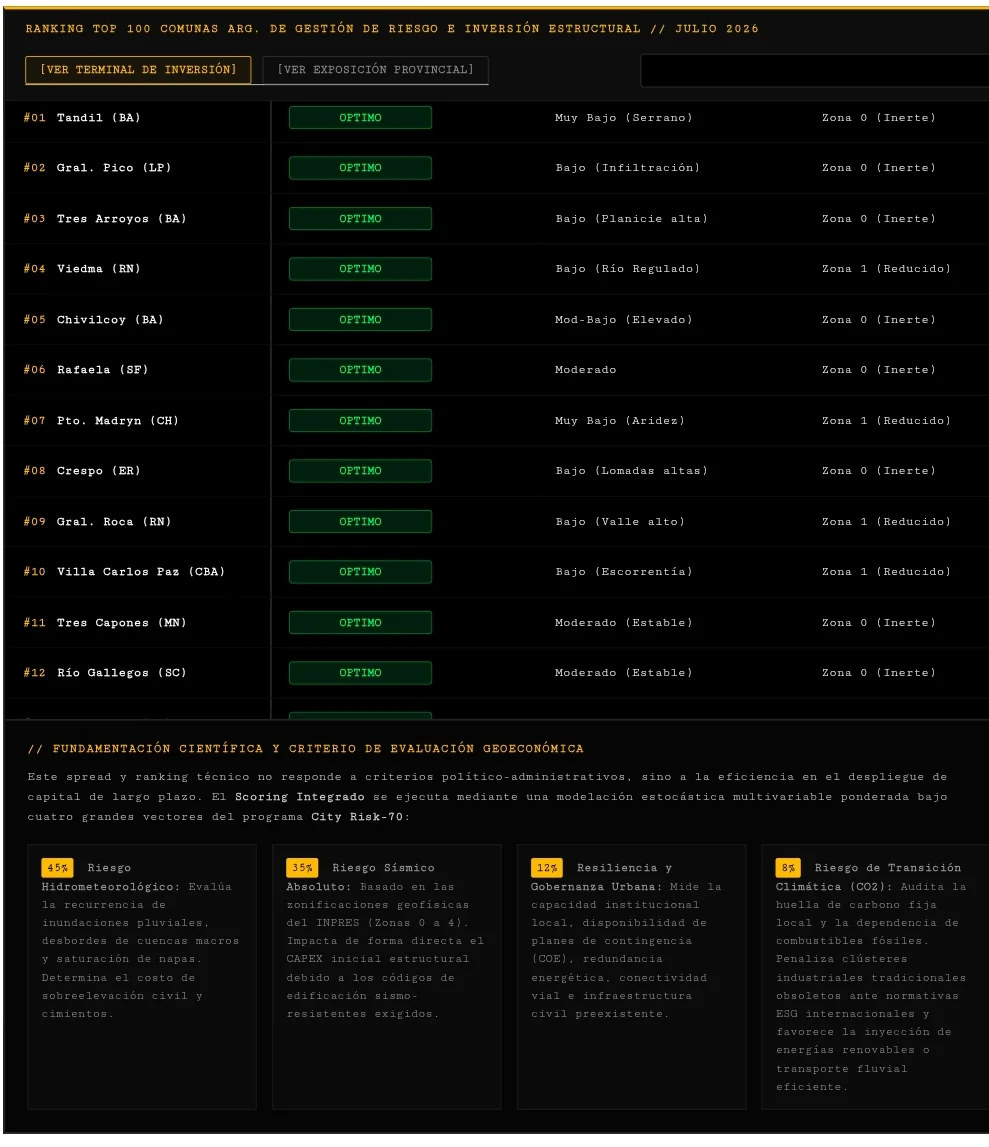

Innovación en métricas territoriales y corporativas: el portal Risk News lanza rankings dinámicos junto al Foro de las Américas

RN

Ciencia e Innovación27 de julio de 2026La plataforma desarrollada en el marco del Programa City Risk-70 introduce un modelo analítico interactivo que actualiza mensualmente el desempeño de empresas iberoamericanas, ciudades para la inversión y parques industriales en Argentina.

El experimento de frenar la inmigración en el Reino Unido: Lecciones de riesgo operativo y económico para 2026

RN

Gestión de Riesgos Migratorios27 de julio de 2026A mediados de 2026, el desplome del 81% en la migración neta británica tras las severas restricciones impuestas muestra el lado oscuro de la soberanía fronteriza: escasez crítica de talento, quiebra de universidades y parálisis operacional en el sector asistencial.